💰 Spain’s Net Wealth Tax (Impuesto sobre el Patrimonio) Explained

Understanding the Spanish Net Wealth Tax (Impuesto sobre el Patrimonio) is a crucial aspect of financial planning for anyone with significant assets in Spain or globally if they become a tax resident.

🏛️ Administration and Regional Power

The Wealth Tax is a state-level tax, but its management and collection are highly decentralized:

- Management: 100% of the revenue from the Wealth Tax is transferred to the Autonomous Communities (Spain’s regional governments).

- Regional Power: The Autonomous Communities hold the authority to set their own rules for the minimum tax exemption (mínimo exento), the applicable tax rates (tipos impositivos), and any bonuses or deductions.

- State Default: Should a Community choose not to establish its own rules, the general state rules apply by default.

🙋 Filing Requirement: The Minimum Exemption

An individual is obligated to file a Wealth Tax return if their gross assets (total value of assets before deducting debts) are valued at more than the minimum tax-exempt amount (mínimo exento).

- General State Minimum: Where the regional government has not set a specific amount, the minimum exemption is €700,000.

- Taxable Wealth: The tax is applied only to the portion of your net worth (assets minus debts and the minimum exemption) that exceeds this threshold.

- Primary Residence Exemption: Your primary residence is exempt up to a maximum of €300,000. This exemption is in addition to the minimum exempt amount.

Mínimo Exento in Key Autonomous Communities

The table below highlights the minimum exemption thresholds set by various Autonomous Communities.

| Autonomous Community | Minimum Exemption (€) | Notes on Disability & Bonuses |

| State Default | 700,000 | Applies where Community hasn’t regulated |

| Andalusia | 700,000 | 100% Bonus in effect (0 tax due) |

| Aragón | 700,000 | |

| Balearic Islands | 3,000,000 | |

| Canary Islands | 700,000 | |

| Catalonia | 500,000 | |

| Extremadura | 500,000 | Higher exemption for registered disabilities |

| Murcia | 3,700,000 | |

| Valencia | 500,000 | Higher exemption (€1,000,000) for certain disabilities |

Tax Guide 2026

If you need an overall view of tax obligations, click on Taxes in Spain Guide 2026.

👤 Scope: Residents vs. Non-Residents

The obligation to declare the tax depends on your tax residency status in Spain on the day the tax is calculated.

- Tax Obligation for Residents (Obligación Personal)If you are a tax resident in Spain, you must declare your total worldwide assets (all assets and rights, regardless of their global location) as they stand on December 31st.

- Tax Obligation for Non-Residents (Obligación Real)If you are not a tax resident in Spain, your obligation is limited to declaring only the assets and rights located, exercisable, or required to be fulfilled within Spanish territory. This includes real estate located in Spain, bank accounts held in Spanish banks, or assets linked to a professional activity carried out here.

🗓️ Calculation Date: The tax liability is always determined based on the value of your wealth as it exists on December 31st of the tax year.

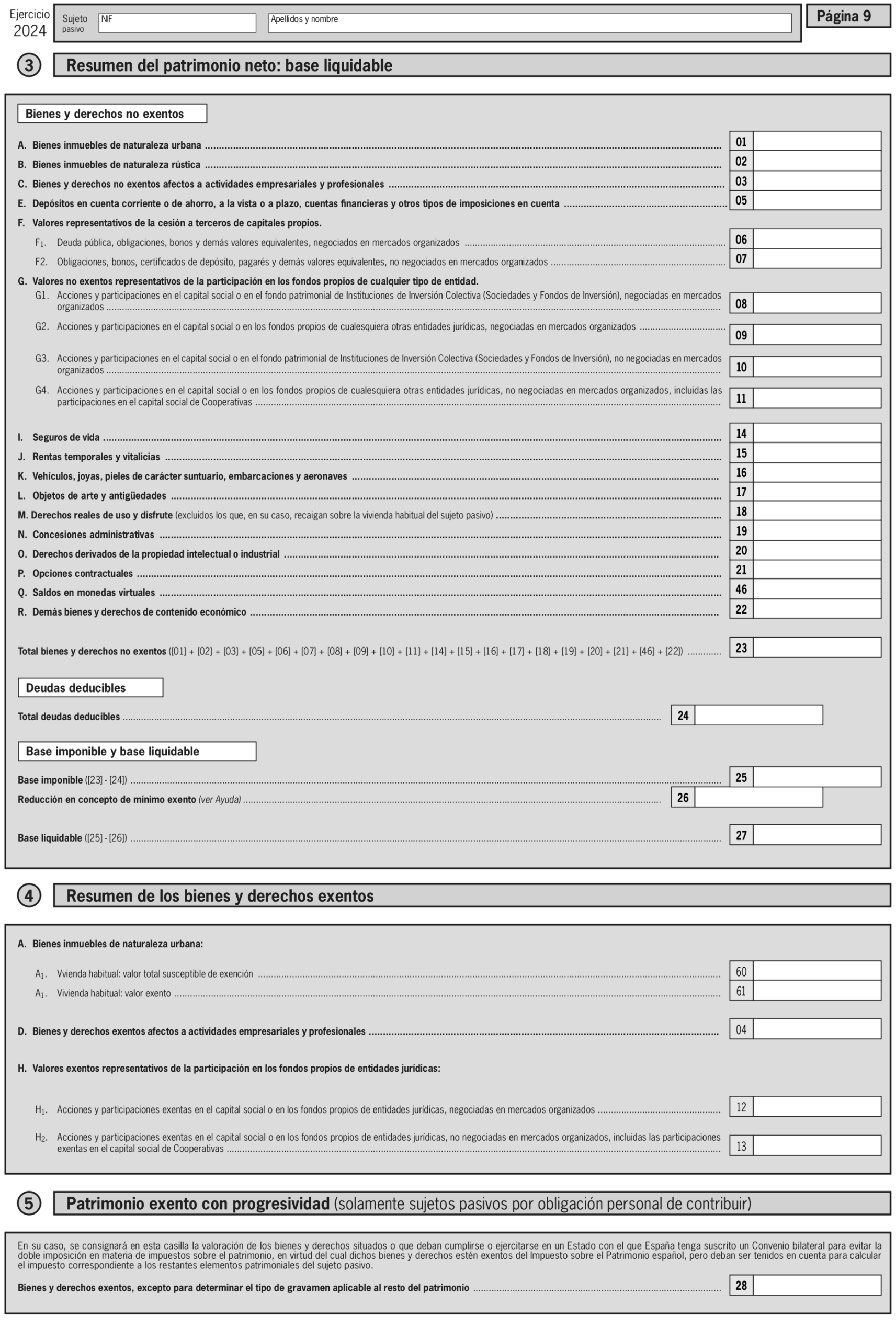

⚖️ Valuing Assets and Deducting Debts

The calculation of your Gross Wealth requires specific valuation rules for different asset classes:

Asset Valuation Rules (Valoración de Bienes)

| Asset Type | Valuation Rule |

| Real Estate (Property) | The highest of these three values: Catastral Value, value set/checked by the tax authority, or Acquisition Price/Value. |

| Bank Deposits (Accounts) | The highest of the balance on December 31st or the average balance of the last quarter of the year. |

| Public Debt/Traded Securities | The average trading price of the fourth quarter of the year. |

| Life Insurance | The surrender value (the cash-out value) on December 31st. |

| Virtual Currencies (Cryptocurrency) | Their value in euros on December 31st. |

| Other Assets | Luxury vehicles, art, jewelry, etc., are valued at their market value on December 31st. |

Deductions for Debts and Charges

You are permitted to deduct debts and personal obligations that you are liable for, as well as real charges and encumbrances (such as mortgages) that reduce the value of specific assets.

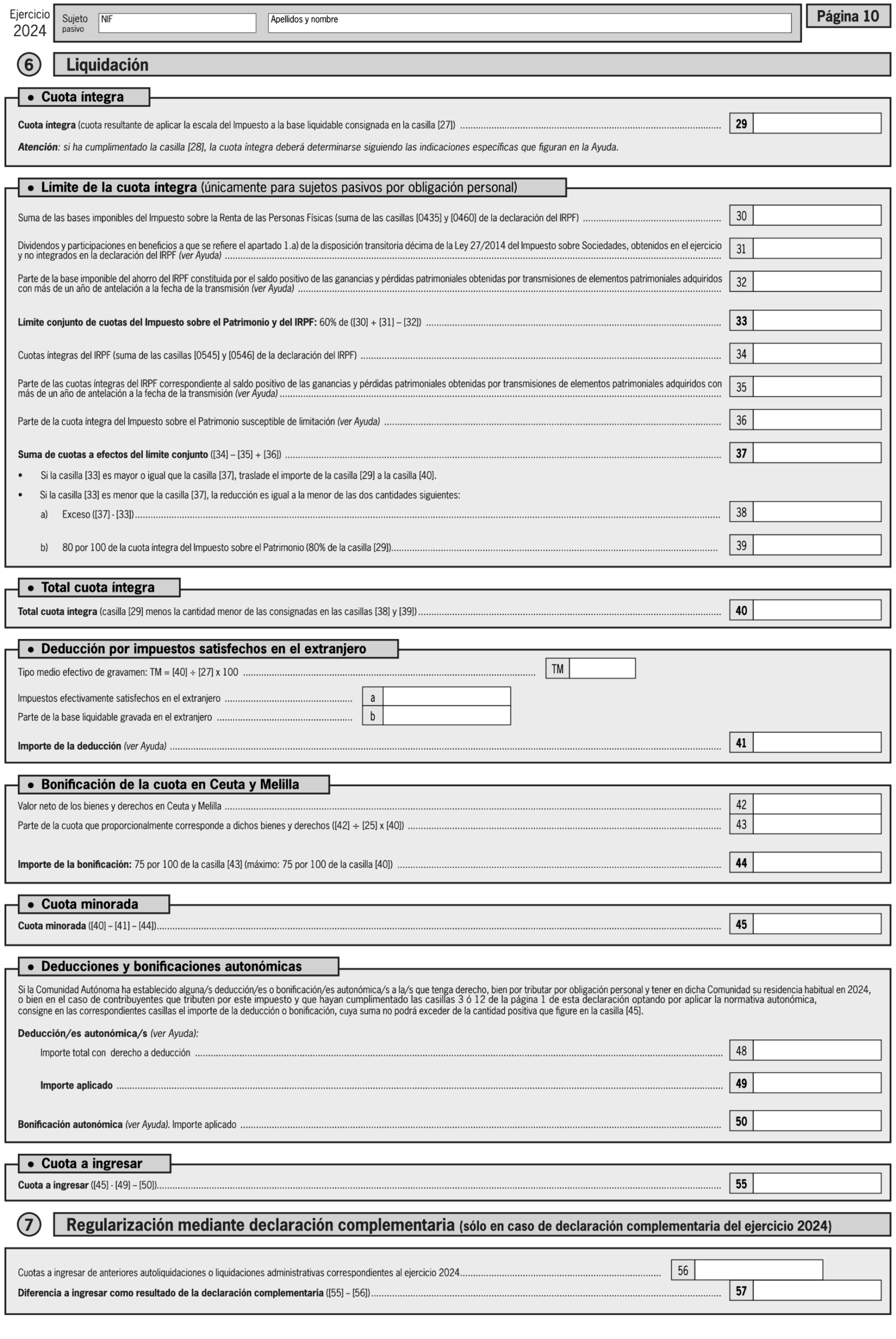

📊 Tax Rates and Progressive Scales

The tax is applied to the Net Taxable Base (Gross Assets – Deductible Debts – Minimum Exemption) using a progressive scale, meaning the tax rate increases as the net wealth amount rises.

Tax Scales: State, Andalusia, and Valencia (Example Rates)

The following partial table shows how regional governments can set their own progressive scales.

| Taxable Base (€) | State Rate (%) | Andalusia Rate (%) | Valencia Rate (%) |

| Up to 167,129.45 | 0.20% | 0.20% | 0.25% |

| From 167,129.45 to 334,252.88 | 0.30% | 0.30% | 0.37% |

| From 334,252.88 to 668,499.75 | 0.50% | 0.50% | 0.62% |

| Over 10,695,996.06 | 3.50% | 3.50% | 3.50% |

🎁 Important Note on Bonuses: Some Autonomous Communities, most notably Andalusia, have implemented a 100% bonus on the tax quota. This means that although residents must file the return, the amount payable is zero.

💡 Calculation Example: Determining Final Tax Due

The calculation uses the Net Taxable Base but incorporates the value of certain exempt assets (like the primary residence exemption) into the process to determine the applicable average tax rate (progressivity).

| Data (Hypothetical) | Value (€) |

| A: Net Taxable Base (After debts and minimum exemption) | 356,900 |

| B: Exempt Assets (Used for rate calculation only, e.g., primary home) | 68,000 |

- Determine the Base for Rate Calculation: Sum the Net Taxable Base (A) and Exempt Assets (B):

- 356,900 + 68,000 = 424,900

- Apply the Tax Scale (State Example):

- Tax on first €334,252.88: €835.63

- Remaining base (€90,647.12) taxed at 0.50%: 90,647.12 * 0.0050 = €453.24

- Total Tax Resulting: €835.63 + €453.24 = €1,288.87

- Calculate the Average Tax Rate (TMG): Divide the Total Tax Resulting by the Rate Calculation Base:

- TMG = (1,288.87 / 424,900) * 100 = 0.3033%

- Calculate the Total Tax Due (Cuota Íntegra): Apply the final average rate only to the Net Taxable Base:

- Cuota Íntegra = 356,900 * 0.003033 = €1,082.26

📄 Need an official form? > You can download the reference PDF and other tax models in our Spanish Tax Forms Library. We provide summaries and official BOE templates to help you prepare your filing.

{kind=link}

{kind=link}

{kind=link}

{kind=link}