The US Citizen Tax Checklist: Dual Filing and Compliance in Spain

As a U.S. citizen or Green Card holder residing in Spain, you face unique tax complexity: you are taxed on your worldwide income by both the Spanish (AEAT) and U.S. (IRS) governments. The key to financial well-being is using the U.S.-Spain Tax Treaty and specific U.S. forms to prevent paying tax twice.

🔑 Phase 1: Dual Compliance (The U.S. Annual Filing)

This is the U.S. side of the filing, generally due to the IRS by June 15th (with an extension available to October 15th).

| Task | U.S. Form / Obligation | Deadline | Focus & Implication |

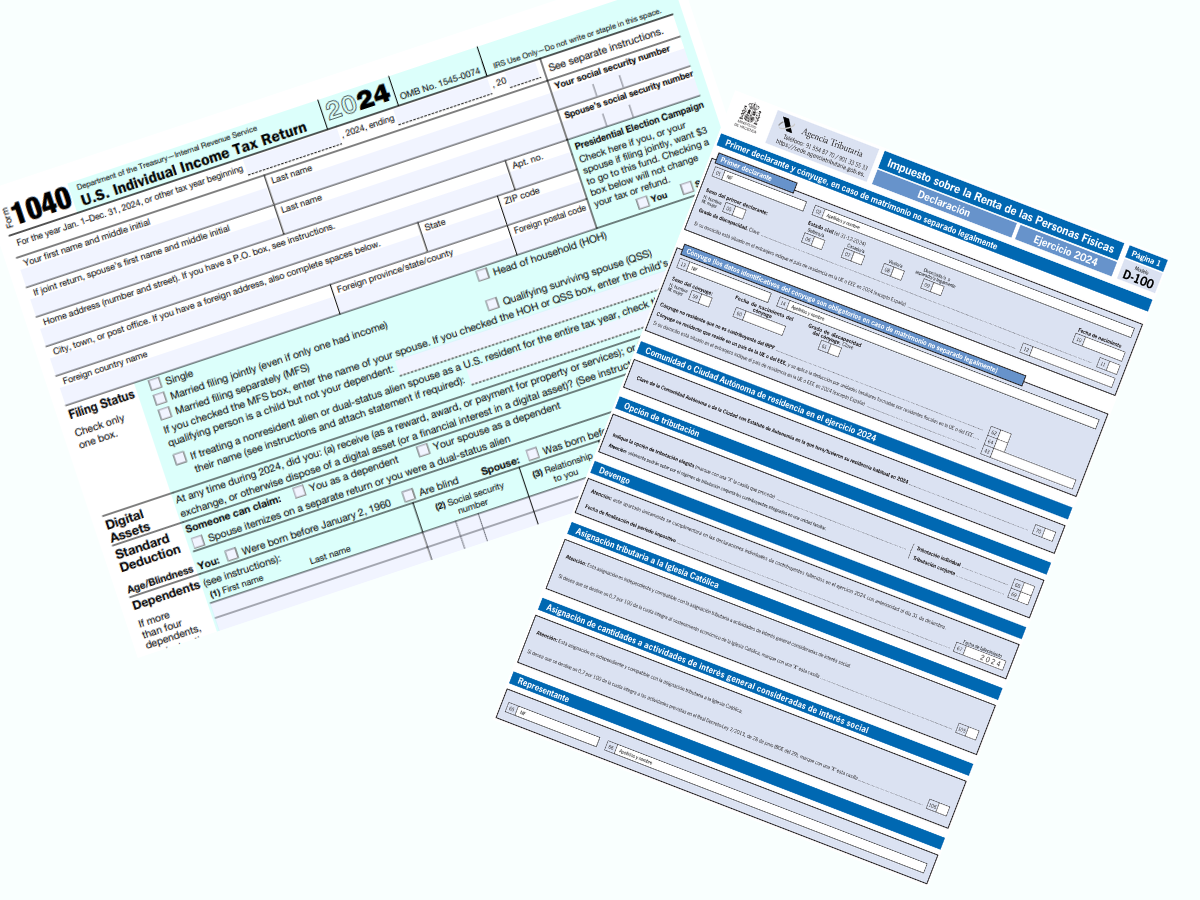

| 1. Federal Income Tax Return | Form 1040 | April 15 (automatic extension to June 15 for expats). | Declares worldwide income in U.S. dollars. This is the starting point for all other forms. |

| 2. Avoid Double Taxation | Form 1116 (Foreign Tax Credit – FTC) | Filed with Form 1040. | The primary method for U.S. expats in Spain. It provides a dollar-for-dollar credit for income tax paid to the AEAT against your U.S. tax liability. |

| 3. Declare Foreign Accounts | FBAR (FinCEN Form 114) | April 15 (automatic extension to October 15). | Mandatory if the aggregate maximum balance of all foreign financial accounts exceeds $10,000 at any time during the year. Filed electronically with FinCEN, not the IRS. |

| 4. Declare Foreign Assets (FATCA) | Form 8938 | Filed with Form 1040. | Mandatory if specified foreign financial assets (accounts, investments, foreign pensions) exceed: $200,000 (Single) or $400,000 (Married Filing Jointly) on the last day of the year. |

| 5. Tax Treaty Position (If Needed) | Form 8833 | Filed with Form 1040. | Used to formally declare a position based on the U.S.-Spain Tax Treaty, such as non-taxability of certain public pensions. |

🇪🇸 Phase 2: Spanish Compliance (As a Tax Resident)

This is the Spanish side of the filing, declaring your worldwide income in Euros to the AEAT.

| Task | Spanish Form / Obligation | Deadline | Focus & Implication |

| 1. Annual Income Tax Return | Modelo 100 (IRPF) | April to June of the following year. | Declares worldwide income in Spain. U.S. Social Security benefits and retirement distributions are generally taxable as ordinary income in Spain. |

| 2. Foreign Asset Declaration | Modelo 720 | January 1st to March 31st annually. | Mandatory if foreign assets (including U.S. bank/brokerage accounts) exceed €50,000 in three categories. Note: Some U.S. retirement accounts (like 401(k)s) are often exempt until funds become accessible. |

| 3. Wealth Tax Check | Modelo 714 | April to June annually. | Required if worldwide net assets (including U.S. retirement funds, real estate) exceed the regional threshold (often €700,000). The US-Spain DTA does not exempt assets from this tax. |

Tax Guide 2026

If you need an overall view of tax obligations, click on Taxes in Spain Guide 2026.

📄 Need an official form? > You can download the reference PDF and other tax models in our Spanish Tax Forms Library. We provide summaries and official BOE templates to help you prepare your filing.