🇪🇸🇬🇧 Spain-UK Double Taxation Treaty: Key Forms for Residents

The Double Taxation Convention (DTC) between Spain and the United Kingdom is a critical agreement for individuals and companies with financial ties to both countries. Its primary purpose is to prevent the same income from being taxed in both jurisdictions, ensuring that taxpayers are aware of where they are liable to pay tax and at what rate.

For Spanish residents receiving UK-sourced income—such as dividends, interest, royalties, or pensions—the treaty allows them to apply for reduced withholding tax at the source (in the UK) or claim a tax credit/refund in Spain. This process relies heavily on specific forms provided by the tax authorities of both countries.

Informative content regarding the Spain-UK Double Taxation Treaty: specific, operational details about the forms used by the Spanish Tax Agency (Agencia Tributaria) and HMRC (UK tax authority) to implement the treaty.

Implementing the Treaty: Essential Forms and Procedures

The forms listed below, primarily derived from the Order of September 22, 1977, are used by the Spanish Tax Agency (Agencia Tributaria) to allow Spanish residents (individuals and companies) to claim the relief granted by the treaty, particularly concerning UK-sourced dividends, interest, royalties, and pensions.

1. Forms for Claiming Tax Credits on UK Dividends

These forms are used to claim payment of the excess tax credit available on British-sourced dividends obtained by a resident in Spain.

- SPA/INDIVIDUAL/CREDIT: Used by a Spanish resident individual to request payment of the excess tax credit applicable to UK-sourced dividends.

- SPA/COMPANY/CREDIT: Used by a Spanish resident legal entity (company) to request payment of the excess tax credit applicable to UK-sourced dividends.

2. Forms for Claiming Relief on Interest, Royalties, and Pensions

These forms allow Spanish residents to request a reduction, refund of excess tax withheld, or exemption on income like interest, royalties, and pensions originating from the UK.

- SPA/INDIVIDUAL: Used by a Spanish resident individual to request a reduction or refund of excess tax paid on UK-sourced interest or royalties, or to claim exemption on pensions or annuities.

- Note on Updates: The UK tax authorities (HMRC) have revised this form. The new version replaces the old one and is available on HMRC’s website.

- SPA/COMPANY: Used by a Spanish resident legal entity (company) to request a reduction or refund of excess tax paid on UK-sourced interest or royalties.

- Note on Updates: Like the individual form, the UK authorities have also revised this form.

http://www.hmrc.gov.uk/cnr/spain-individual.pdf

http://www.hmrc.gov.uk/cnr/spain-company.pdf

3. UK-Specific Forms and Procedural Updates

The UK tax authority, HMRC, also provides forms that Spanish residents must use to apply for tax relief at the source in the UK.

| Form | Purpose (Applicant: Spanish Resident) | Important Procedural Note |

| UK-REIT (Real Estate Investment Trust DT-COMPANY) | Used to claim UK tax refunds on dividends paid by UK-REITs. | Requires certification regarding fiscal residence and subjection to tax. |

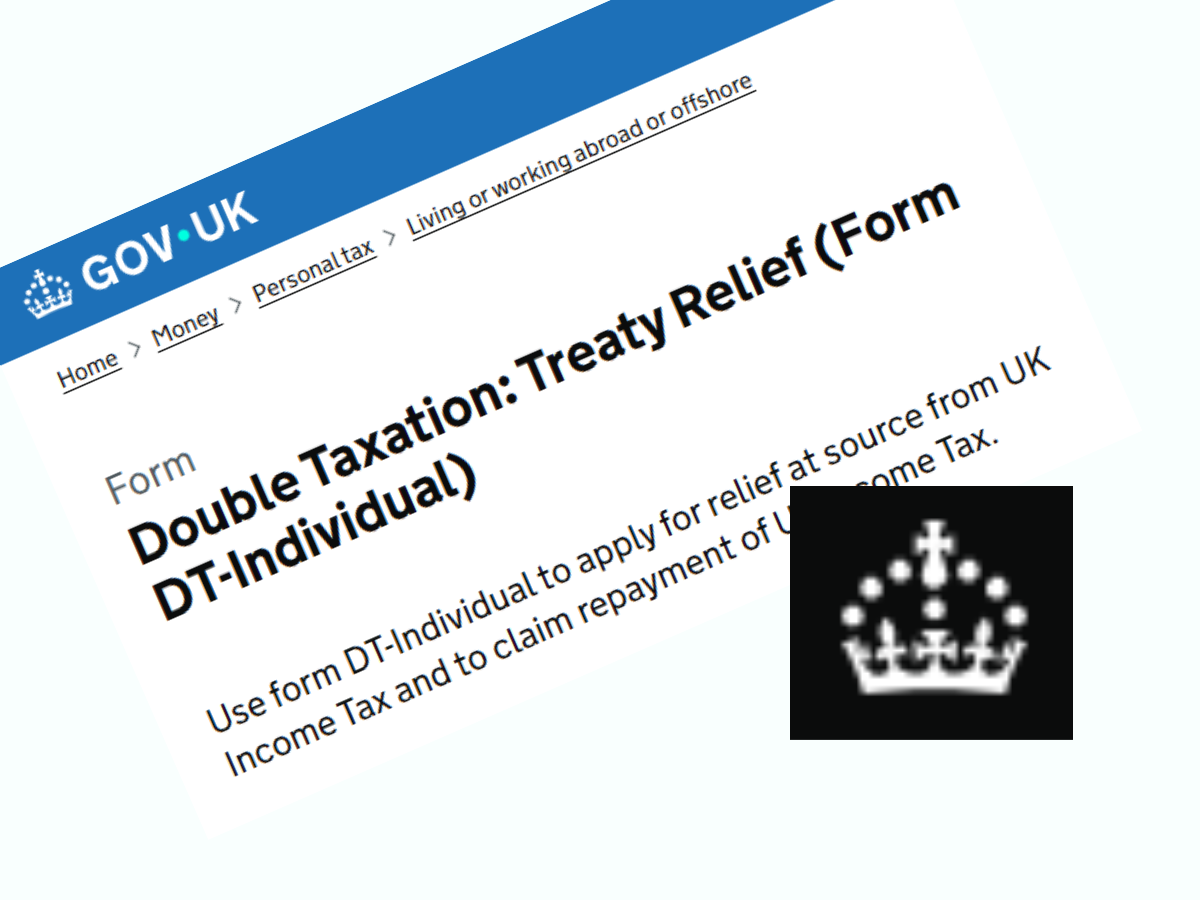

| Form DT-Individual | Application for relief at source from UK Income Tax and claim for repayment of UK Income Tax on pensions, annuities, interest, and royalties. | Requires certification regarding residence under the Convention and subjection of the income to tax (can be processed). |

| Formulario España-individual (Spain-individual) | Application for relief at source from UK Income Tax and claim for repayment of UK Income Tax for an individual receiving pensions, annuities, interest, or royalties from the UK. | IMPORTANT NEW PROCEDURE: The certification previously contained within the form has been replaced. The taxpayer must now request the specific Spanish Tax Agency certificate called “Residencia fiscal en España. Convenio” and attach it to this UK form. |

4. EU Directives and Cross-Border Interest/Royalties

The Directive 2003/49/CE (regarding the common tax regime for interest and royalty payments between associated companies in different EU Member States) may also apply.

- A specific EU Claim Form is available from HMRC for this purpose.

- Note: The Spanish tax authority has stated that while the form is not translated into Spanish, it can still be completed and submitted. A translation may be requested if the document is presented exclusively in English, as per Spanish regulations (Order HAC/3626/2003).

Conclusion and Disclaimer

Navigating international tax treaties requires careful attention to deadlines and proper documentation. The periodic revisions to these forms, such as the change in the certification requirement for the Formulario España-individual, underscore the need to always use the latest versions available from the official websites of the Spanish Tax Agency and HMRC.