Spain’s Tax Common vs. Foral Regimes

Spain does not have a single, unified tax system. Understanding the difference between the Common Regime (Régimen Común) and the Foral Regime (Régimen Foral) is crucial, as your tax obligations and the rates you pay depend heavily on your region of residence.

🏛️ The Common Regime (Most Autonomous Communities)

This regime applies to the vast majority of Spain’s Autonomous Communities (CC.AA.). Under this system, the Central Administration (the State, primarily through the AEAT—Agencia Estatal de Administración Tributaria) plays the main role in revenue collection.

How It Works

- Central Collection: The State collects taxes to fund its national services and transfers funds to the CC.AA. for their decentralized services (like health and education).

- Tax Transfers ($Tributos Cedidos$): The State transfers legislative and collection powers for certain taxes to the CC.AA. This ability to modify rates and deductions is what leads to the significant tax variations between regions.

📝 Key Taxes and Jurisdiction

| Tax | State Competence | Autonomous Community (CC.AA.) Competence |

| Personal Income Tax (IRPF) | State rates and rules (approx. 50% of tax base) | Regional rates and rules (approx. 50% of tax base) |

| Wealth Tax (I. Patrimonio) | General rules | Rates, deductions, and exemptions (e.g., minimum exempt amount) |

| Solidarity Tax on Large Fortunes | State rules and collection | None (A State tax) |

| Inheritance & Gift Tax (I. Sucesiones y Donaciones) | Minimum national rules | Vast legislative power (Leads to huge differences in rates and bonuses) |

| Corporate Tax (I. Sociedades) | Full State competence | None (Except specific regional adjustments) |

In addition to the above, CC.AA. have the power to create and levy some minor regional taxes (e.g., environmental taxes).

🌴 The Special Case of the Canary Islands

Within the Common Regime, the Canary Islands possess a special Economic and Fiscal Regime (REF). This is due to historical and geographical reasons and is regulated according to EU provisions for outermost regions. This allows for specific incentives and tax benefits (like the IGIC—a local indirect tax instead of VAT).

🏔️ The Foral Regime (Basque Country & Navarre)

The Foral Regime applies only to the Basque Country (País Vasco) and the Foral Community of Navarre (Comunidad Foral de Navarra).

How It Works

This system is characterized by a high degree of fiscal autonomy granted by their respective Concierto (Economic Agreement) and Convenio (Economic Convention).

- Legislative Power: These regions have the power to maintain, establish, and regulate their own tax legislation, including the full scope of IRPF, VAT, Corporate Tax, etc. They essentially draft their own tax laws.

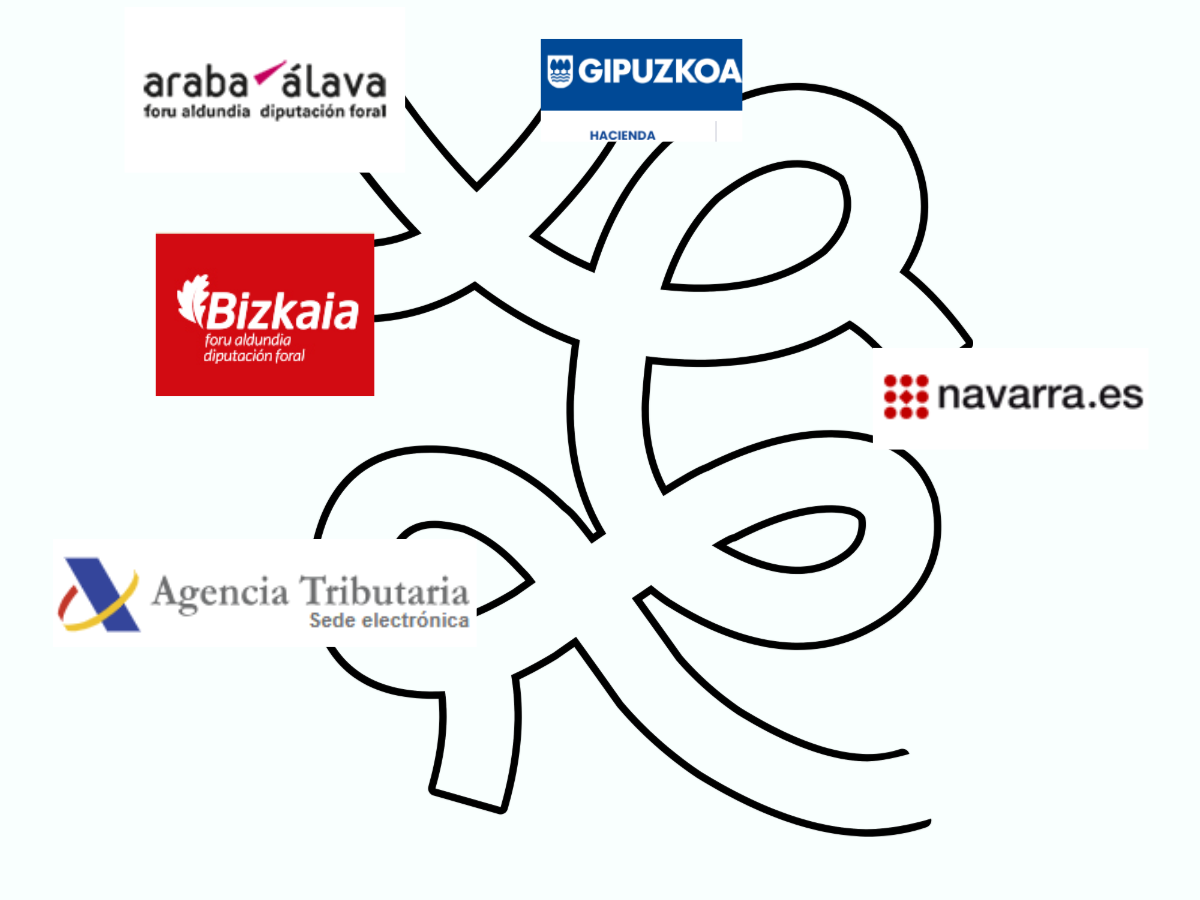

- Direct Collection: The Foral Territories collect all the taxes directly through their own tax agencies:

- Navarre: Has its own separate Tax Agency (Hacienda Foral de Navarra).

- Basque Country: This is further divided into three separate tax offices (Haciendas Forales)—one for each of its three provinces (Álava, Biscay, and Gipuzkoa).

- The Quota (Cupo): They contribute a fixed, annual amount (known as the Cupo or Aportación) to the Central State to finance common national services (such as defense, foreign affairs, and infrastructure).

❓ How This Affects Residents in Spain

The existence of these two models and regional differences has a direct impact on the taxpayer’s wallet and compliance process.

A. Substantive Differences (What You Pay)

The legislative independence leads to different tax burdens in each region:

- IRPF: The regional portion of your income tax rate and certain personal deductions are set by your Autonomous Community.

- Wealth & Inheritance Taxes: These are the most divergent taxes. For example, some CC.AA. offer near-total Inheritance and Gift Tax relief, while others maintain high rates. The rules depend entirely on the CC.AA. where you are a tax resident.

Note: Many autonomies use the State legislation as a base and only apply minor modifications; however, the trends show increasing divergence.

B. Procedural Differences (How You File)

Your region of residence determines where and how you file:

- Common Regime Residents: You file most major taxes (like IRPF) with the AEAT (State Tax Agency), although the CC.AA.’s rules are applied to the regional portion of your return.

- Foral Regime Residents: You file directly with the specific regional tax authority (Hacienda Foral of Navarre, Gipuzkoa, etc.) using their own specific forms, deadlines, offices, and help services. The AEAT is not involved in your main tax filings.

Understanding your tax domicile (domicilio fiscal)—the CC.AA. where you spend most of the year—is the first and most critical step in managing your Spanish taxes.