Tax Residency in Spain: A Guide for Expats

Determining your tax residency is the single most important step in understanding your obligations in Spain. The rules decide whether you pay tax on your worldwide income or only on what you earn within Spain.

If you’re unsure where to begin, check out our comprehensive tax obligation strategy. Taxes in Spain Guide 2026.

Spanish law uses a series of tests to establish residency. You are considered a Spanish tax resident if you meet any of the following criteria:

The Three Tests for Spanish Tax Residency

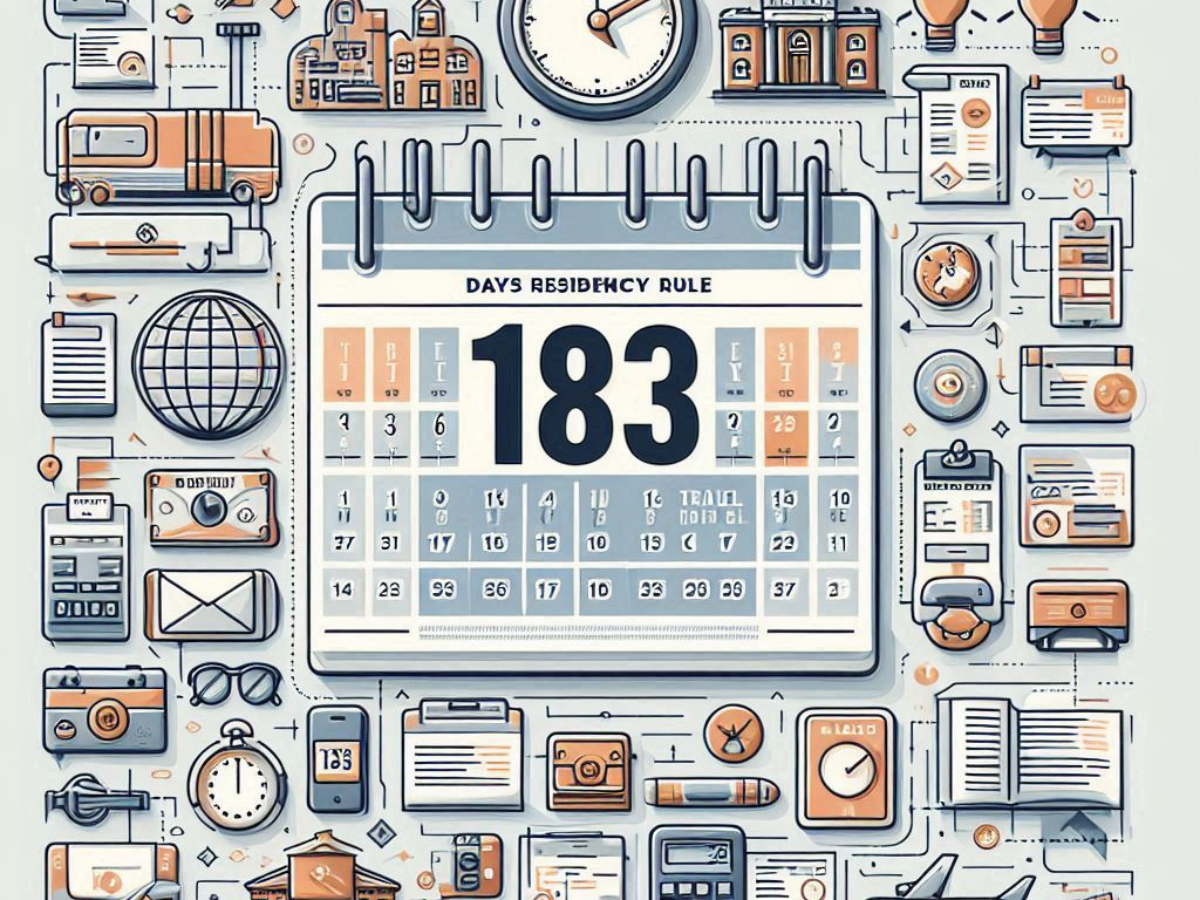

1. The 183-Day Rule (The Bright-Line Test)

This is the most straightforward rule. You are a tax resident if you spend more than 183 days in Spain during a calendar year.

- Key Detail: Sporadic absences count as time in Spain. The burden is on you to prove you were resident elsewhere if you claim to be non-resident.

- How to Prove Your Stay: The tax authorities can consider a wide range of evidence, including your padrón certificate, rental contract, work contract, school enrollments for children, or even passport stamps.

2. The Center of Vital Interests Test (The Economic & Personal Tie-Breaker)

You can be deemed a tax resident if the main base or core of your economic activities or interests is in Spain. This is a broader concept that looks at:

- Where your primary professional, business, or investment income is generated.

- Where your most significant assets are located.

- The country you have the strongest personal and economic ties with.

3. The Family Ties Test (The “Attraction” Rule)

It is presumed that you are a tax resident in Spain if your spouse (not legally separated) and your minor dependent children habitually reside in Spain.

- Evidence to the Contrary: You can challenge this presumption by providing a tax residency certificate from another country or other compelling evidence.

Notice Title

If you need an overall view of tax obligations before digging into this specific topic, click on Taxes in Spain Guide 2025

Tie-Breakers: The Double Taxation Treaty (DTA) Solution

What if you could be considered a tax resident in both Spain and your home country? This is where Double Taxation Agreements (DTAs) come in. Spain’s treaties follow international models to resolve this conflict with a step-by-step tie-breaker:

- Permanent Home: You are a resident of the country where you have a permanent home available to you.

- Center of Vital Interests: If you have a home in both, it’s the country with which you have closer personal and economic relations.

- Habitual Abode: If that is unclear, it’s the country where you have a “habitual abode” (i.e., you live more regularly).

- Nationality: If you live in both or neither, it’s the country of your nationality.

- Mutual Agreement: If all else fails, the tax authorities of the two countries will decide for you.

The Key Date: Understanding July 2nd

July 2nd is the 183rd day of the year. This date is a critical practical reference:

- If you arrive in Spain before July 2nd with the intent to stay, you will likely become a tax resident in that same year.

- If you leave Spain before July 2nd to reside elsewhere, you will likely become a non-resident for that entire year.

- You must report a change of tax residency using the Form 030.

Tax Residency Certificate

- To Prove Residency in Spain: You can request a certificate from the Spanish Tax Agency (Agencia Tributaria). It is typically valid for one year and requires you to be registered as a resident and have a tax history in Spain.

- To Prove Residency Elsewhere: The best way to prove you are a tax resident of another country (e.g., to challenge the family ties rule) is to provide an official certificate from that country’s tax authority.

The Future: The FASTER Directive (Coming in 2030)

Adopted in 2024, the FASTER Directive will modernize tax procedures within the EU starting in 2030. Its key features include:

- Digital Tax Residency Certificates (e-CDRF): A fully digital and standardized process.

- Faster Refunds: Obliges countries to process withholding tax refunds within 60 days.

- Anti-Abuse Rules: New reporting requirements to prevent fraudulent claims. This will make the system more efficient and transparent for compliant taxpayers.

LEGAL FRAMEWORK:

Ley 35/2006, de 28 de noviembre, del Impuesto sobre la Renta de las Personas Físicas, Law 35/2006, of November 28, on the Personal Income Tax.

Article 9. Taxpayers who have their habitual residence in Spanish territory.

1.A taxpayer shall be deemed to have their habitual residence in Spanish territory when any of the following circumstances apply:

a) They spend more than 183 days, during the calendar year, in Spanish territory. To determine this period of stay in Spanish territory, sporadic absences shall be included, unless the taxpayer proves their tax residence in another country. In the case of countries or territories considered tax havens, the Tax Administration may require proof of stay in that country for 183 days in the calendar year. To determine the period of stay referred to in the previous paragraph, temporary stays in Spain that result from obligations under cultural or humanitarian collaboration agreements, free of charge, with Spanish Public Administrations, shall not be counted.

b) The main core or the base of their activities or economic interests is located in Spain, directly or indirectly. It shall be presumed, unless proven otherwise, that the taxpayer has their habitual residence in Spanish territory when, according to the previous criteria, their spouse not legally separated and their minor dependent children habitually reside in Spain.

2. Due to reciprocity, foreign nationals who have their habitual residence in Spain shall not be considered taxpayers when this circumstance is a result of any of the cases established in Section 1 of Article 10 of this Law and the application of specific norms derived from international treaties to which Spain is a party is not appropriate.