🏛️ The Landmark Schumacker Ruling

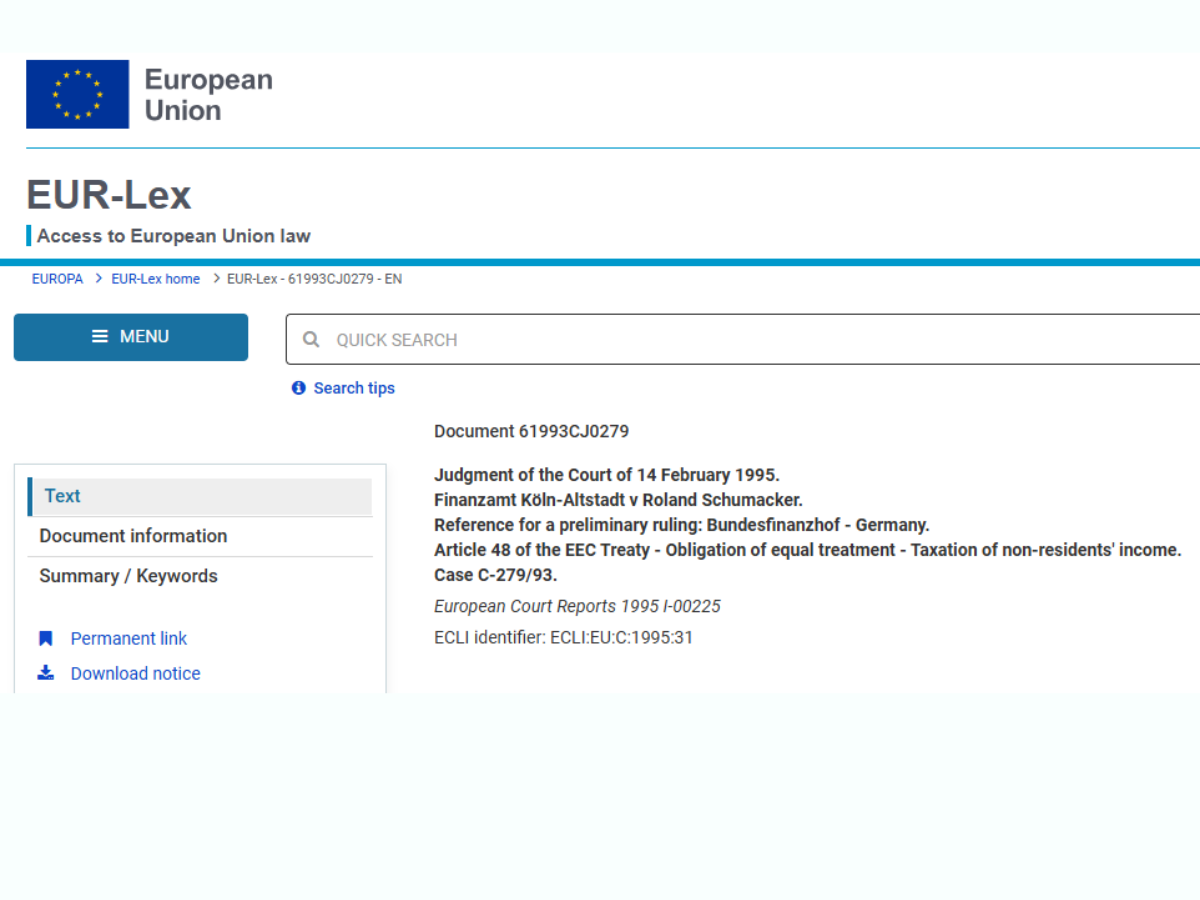

The Schumacker Case (C-279/93) is a foundational pillar of European Union tax law, fundamentally altering how EU member states must treat non-resident workers who earn their livelihood almost entirely within that state. The principles established in this 1995 ruling have a direct and practical impact on tax regimes, including Spain’s distinction between resident and non-resident taxation.

Case Background

The case involved Roland Schumacker, a Belgian national who lived in Belgium but worked in Germany. Under German tax law at the time, he was taxed as a non-resident, which subjected him to a simplified, but often higher, limited tax regime. Crucially, as a non-resident, he was denied the benefit of tax deductions, allowances, and preferential tariffs (like the “splitting tariff” for married couples) that were available to German residents. This was a significant disadvantage, as nearly all of his household’s income was earned in Germany, making Germany the only state capable of taking his personal and family circumstances into account for taxation.

The Central Principle

The European Court of Justice (ECJ) ruled on February 14, 1995, that this difference in treatment constituted discrimination under EU law.

The Court held that while the general distinction between residents (taxed on worldwide income, benefiting from allowances) and non-residents (taxed only on source income, often without allowances) is permissible, this distinction breaks down when a non-resident is in a comparable situation to a resident.

The core finding: It is discriminatory to deny a non-resident worker tax deductions and allowances available to a resident if that non-resident earns “all or almost all” of their worldwide income in the source state.

In such cases, the source state (Germany) is the only state with the ability to grant the necessary tax relief based on the taxpayer’s overall ability to pay and personal circumstances. The residence state (Belgium) cannot do so because the taxpayer lacks sufficient taxable income there.

🇪🇸 The Schumacker Rule in Spanish Tax Law

The Schumacker ruling did not create a new Spanish tax law, but it mandated the principle of non-discrimination for cross-border workers, which Spain was obligated to implement for EU/EEA citizens.

IRPF vs. IRNR

The ruling directly addresses the differences between Spain’s two main tax regimes for individuals:

| Regime | Status | Tax Base | Personal Allowances/Deductions |

| IRPF | Tax Resident | Worldwide Income | Full access to Personal and Family Minimums, deductions, and progressive rates. |

| IRNR | Tax Non-Resident | Spanish-Source Income Only | Generally, limited or no access to personal allowances and deductions (taxed at a flat rate on gross income). |

The Optional Regime (The Schumacker Rule)

Spain codified the Schumacker principle by creating an Optional Tax Regime under the Non-Resident Income Tax (IRNR) Law. This regime allows qualifying EU/EEA non-residents to be treated similarly to Spanish residents.

Who Qualifies? (Key Requirements)

To opt into this regime, the non-resident must be a tax resident of an EU or EEA country (not a tax haven) and meet one of two income tests:

- The 75% Rule (Most Common): The taxpayer must prove that they earned at least 75% of their total worldwide income (from both employment and economic activities) in Spanish territory during the tax year.

- The Low Non-Spanish Income Rule: The Spanish income must be less than 90% of the personal and family tax-exempt minimum of a resident, AND the income earned outside of Spain must also be below that same minimum personal and family threshold.

The Benefit: Non-Discrimination

By opting for this regime, the non-resident gains the most significant benefit of the Schumacker ruling: access to the tax benefits normally reserved for Spanish residents, including:

- Personal and Family Minimums: These allowances (tax-exempt minimums) significantly reduce the income subject to tax, lowering the effective tax burden.

- Standard Deductions: Eligibility for deductions related to personal circumstances and family dependents.

How the Tax is Calculated

The taxpayer does not actually switch to IRPF. Instead, they declare under IRNR, but the tax is calculated using the IRPF rules:

- The Tax Agency calculates the average rate of IRPF based on the taxpayer’s entire worldwide income and personal/family circumstances.

- This average rate is then applied only to the portion of the income earned in Spanish territory.

- The final result often leads to a refund of the excess tax initially paid through withholdings under the standard IRNR flat rate.

⚖️ Implications Beyond Employment

While the Schumacker case focused on the free movement of workers (Art. 45 TFEU), its principle of non-discrimination has been widely applied to other EU freedoms, particularly the free movement of capital (Art. 63 TFEU), affecting areas like rental income and investment:

- Non-EU Rental Income Deductions: Recent Spanish court rulings (though sometimes subject to appeal) have applied EU principles to grant non-EU non-residents (e.g., US, UK post-Brexit citizens) the right to deduct legitimate expenses against Spanish rental income under IRNR. This parity in deductions directly stems from the non-discrimination philosophy established by Schumacker.

The Schumacker rule remains a powerful instrument that allows cross-border workers and, by extension, certain non-resident investors in the EU/EEA to argue for fair and equitable tax treatment, preventing the source state from imposing a disproportionately heavy tax burden without regard for the taxpayer’s overall ability to pay.

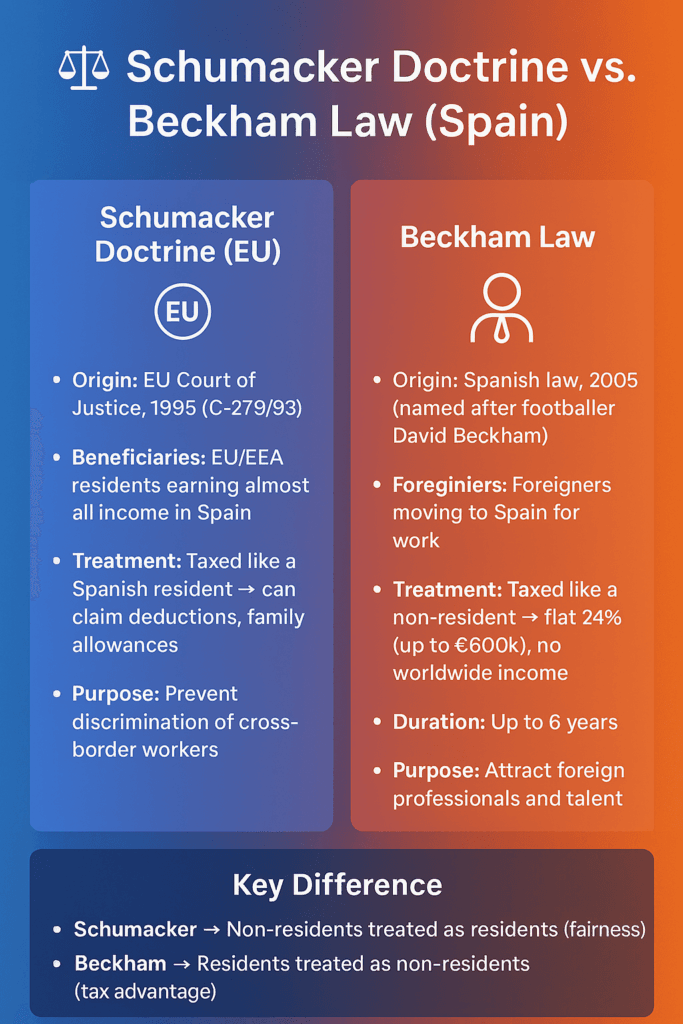

Schumacker Law vs Beckam Law

These are two very different legal concepts in Spain, though they sometimes get confused because both deal with taxation and foreigners.

🔑 Key Differences

| Aspect | Schumacker | Beckham Law |

|---|---|---|

| Type | EU Court doctrine | Spanish national law |

| Who benefits | Non-residents working mainly in Spain (cross-border EU/EEA workers) | Foreigners who move their tax residence to Spain for work |

| Treatment | Treated like a resident → can claim deductions | Treated like a non-resident → flat tax, no worldwide income |

| Purpose | Prevent discrimination | Attract expats and talent |

| Example | A Portuguese living in Portugal but working 90% in Spain | A UK executive relocating to Madrid for 5 years |

👉 In short:

- Schumacker = fairness for cross-border EU workers.

- Beckham = tax incentive for foreign professionals moving to Spain.