Modelo 720/721, Assets and Crypto Located Abroad

Informative declarations are one of the modalities of information gathering that consist of the massive supply of tax-related information to the Administration on a periodic basis and through standardized channels.

- Modelo 720 is the ‘classic’ form. It covers traditional assets like bank accounts, stocks, and real estate.

- Modelo 721 is the newer form specifically for virtual currencies (cryptocurrencies) held in foreign exchanges.

If you’re unsure where to begin, check out our comprehensive tax obligation strategy. Taxes in Spain Guide 2026.

Informative Declaration. Declaration of assets and crypto located abroad exceeding 50,000 Euros, including real estate properties.

- “Informative Declaration.” This specifies that it is for reporting information, not for paying a tax directly (though penalties for not filing can be severe).

- “Assets and rights located abroad.” This is a broad category that includes bank accounts, securities, insurance, and real estate in Modelo 720, cryptocurrencies in Modelo 721.

- Over 50.000 Euros: The filing threshold. You must file if the total value of your declared assets abroad exceeds this amount.

Alert! The 2026 “Zero Opacity” Reality with Modelo 721

In 2026, Modelo 721 (the informative declaration of virtual currencies held abroad) has become one of the AEAT’s most powerful tools for tracking wealth. While Modelo 720 covers traditional bank accounts and property, Modelo 721 is specifically designed for the crypto era.

Under the 2026 guidelines, the “age of anonymity” for crypto in Spain has officially ended due to the integration of the DAC8 Directive and the OECD’s CARF framework.

The biggest shift this year is that the AEAT no longer waits for you to volunteer information. Under DAC8, major exchanges (Binance, Coinbase, Kraken, etc.) are now mandated to automatically report your balances, transaction history, and identity directly to EU tax authorities. If the data they receive from the exchange doesn’t match your Modelo 721, a “parallel assessment” (audit) is triggered automatically.

Key Rules & Fraud Focus Areas for Modelo 721

- The €50,000 “Combined” Trap: You must file if your total crypto held in foreign platforms exceeds €50,000 on December 31st.

- Example: If you have €45,000 in BTC and €6,000 in a stablecoin, you have exceeded the limit and must declare every single asset in your portfolio, even those worth only a few euros.

- The €20,000 Re-filing Rule: If you filed in a previous year, you only need to file again if your total balance has increased by more than €20,000 compared to your last declaration, or if you closed an account/sold a previously declared asset.

- Custodial vs. Self-Custody: * Mandatory: Any crypto on a foreign exchange or “hot wallet” where a third party manages the keys.

- Focus Area: The AEAT is currently debating the status of Cold Wallets (Ledger/Trezor). While technically “self-custody,” the agency is using purchase records and exchange transfer histories to “assume” the existence of these assets if they see large outflows from exchanges to private addresses.

- Exit Tax Scrutiny: For expats planning to leave Spain in 2026, the AEAT is cross-referencing Modelo 721 with “Exit Tax” obligations. If your global portfolio is significant, they will ensure you don’t “disappear” without paying capital gains on the latent increase in your crypto’s value.

Penalties & Deadlines

- Deadline: January 1st to March 31st, 2026.

- Late Filing: €300 minimum fine.

- Incorrect/Omitted Data: €20 per “item” of data (e.g., each coin type or wallet address) omitted or wrong, with a minimum of €300.

- The “Beckham Law” Exception: If you are under the Beckham Law, you are generally exempt from filing Modelo 721 because you are only taxed on Spanish-source income. However, the AEAT is checking if “staking” rewards or “mining” activities could be considered Spanish-source if performed while physically sitting in Spain.

Crucial Warning: Tax vs. Information

Remember, Modelo 721 is only an information form (you pay €0). However, the AEAT uses it to ensure you are paying capital gains (19%–28%) on Modelo 100 (Renta) when you swap or sell.

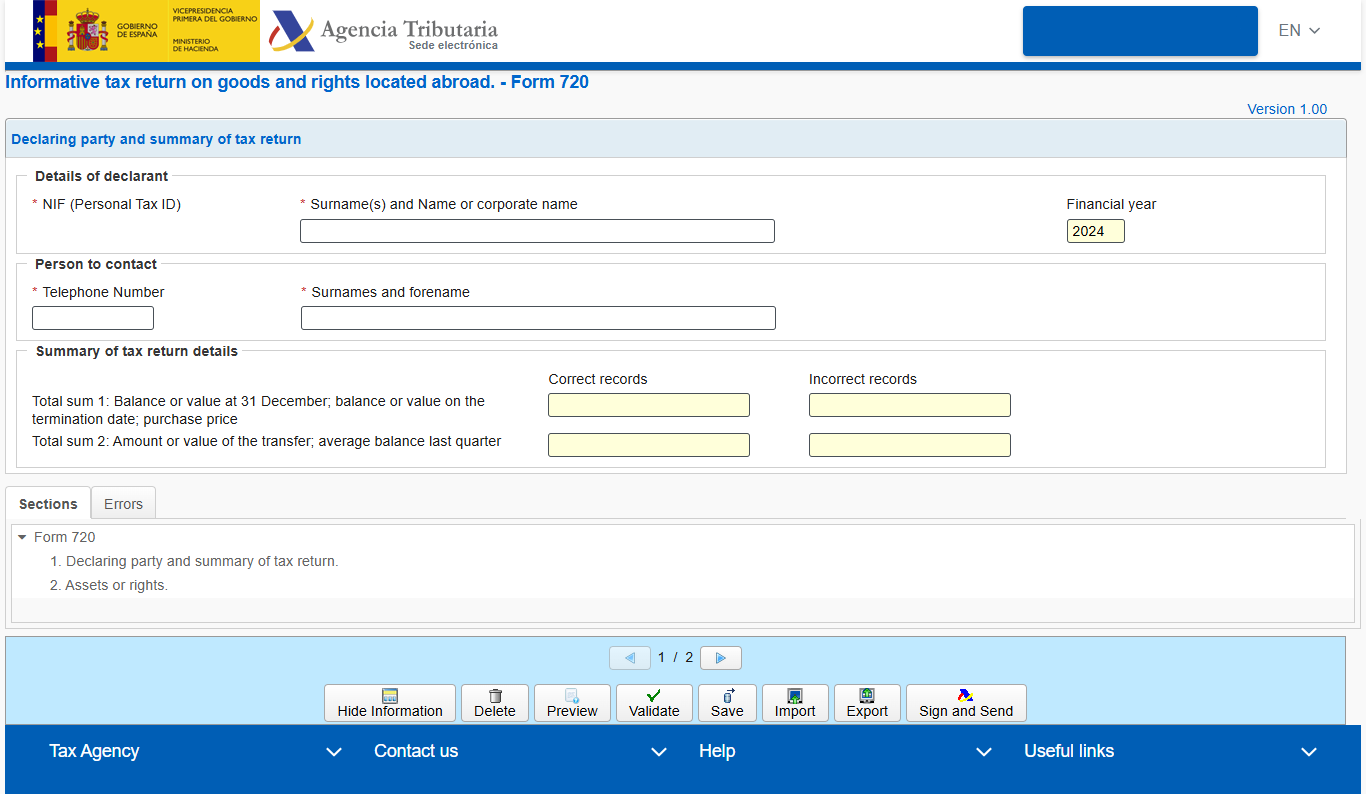

Modelo 720: Assets Abroad Declaration

For Modelo 720, you must file if any of these three categories exceed €50,000 as of December 31st:

- Accounts (Bank balances).

- Investments (Stocks, bonds, life insurance).

- Real Estate (Foreign property).

📄 Need an official form? > You can download the reference PDF and other tax models in our Spanish Tax Forms Library. We provide summaries and official BOE templates to help you prepare your filing.

Modelo 720 FAQ

Any More Questions?

Download here the 21-page PDF.

Current Penalties for Modelo 720 Non-Compliance

The current penalties are complex and depend on whether the filing is late or incorrect, and whether it is done voluntarily or after a request from the Tax Agency (AEAT).

⚠️ Additional Major Consequences

The penalties above are administrative fines. The most significant financial risk comes from the possibility of the Spanish Tax Agency treating the undeclared assets as unjustified capital gains (unjustified wealth):

- Imputed Income: The value of the undeclared asset can be considered as taxable income (unjustified capital gain) for the earliest non-prescribed year, and taxed at the appropriate income tax rate (IRPF).

- Reduced Statute of Limitations: Following the ECJ ruling, the statute of limitations for the Modelo 720 is now generally four years, instead of being open-ended.

- Voluntary Correction: Filing the Modelo 720 voluntarily before an investigation begins is critical for minimizing fines and avoiding the presumption of unjustified capital gains.

Model 721: Declaration on Virtual Currencies Located Abroad

This is a very detailed breakdown of the Model 721 requirements from the Spanish Tax Agency. This information is highly valuable for Spanish tax residents dealing with cryptocurrencies.

1. Who is Obligated to File Model 721?

For Modelo 721, the rules are similar but focused on Crypto. If the total value of your crypto held on foreign exchanges (like Binance, Coinbase, or Kraken) exceeds €50,000 on December 31st, you must file.

Obligation:

- Individuals who are holders of virtual currencies located abroad.

- Individuals who are beneficiaries, authorized persons, or otherwise have power of disposal over virtual currencies.

- Individuals who are the beneficial owners of virtual currencies.

Custody Requirement:

The virtual currencies must be custodied by persons or entities that provide services to safeguard private cryptographic keys on behalf of third parties for the purpose of maintaining, storing, and transferring virtual currencies, as of December 31st each year.

Threshold:

There is no obligation to file if the balances of all virtual currencies held abroad, valued in euros as of December 31st, do not collectively exceed €50,000. If this joint limit is exceeded, information must be provided for all virtual currencies held abroad.

2. What Information Must Be Provided?

The declaration requires the following details for the virtual currencies held abroad:

- The full name or business name, and tax identification number (if applicable), of the person or entity providing custody services for the cryptographic keys (the custodian), along with their address or website address.

- The complete identification of each type of virtual currency.

- The balances of each type of virtual currency as of December 31st, expressed in units of the virtual currency and their valuation in euros.

- Examples of required identification formats include: Bitcoin (BTC), Ethereum (ETH), Tether USDt (USDT), etc., as they appear on reference cryptographic rating sites like CoinMarketCap.

3. Key Definitions and Scope

| Term | Definition and Scope |

| Virtual Currency | A digital representation of value not issued or guaranteed by a central bank or public authority, not necessarily associated with a legally established currency, and lacking the legal status of currency or money, but which is accepted as a medium of exchange and can be transferred, stored, or traded electronically. |

| Situated Abroad | Virtual currencies are considered “situated abroad” when the person, entity, or permanent establishment providing custody services for the private cryptographic keys is not obligated to file an informative declaration in Spain. |

| Custody (Custodial vs. Non-Custodial) | The obligation only applies if the virtual currencies are custodied by a third party. If the holder maintains control of the private cryptographic keys (e.g., in a non-custodial or “cold wallet”), the assets are NOT considered custodied by a third party, and they should not be counted toward the €50,000 reporting threshold for Model 721. |

The “Cold Wallet” Exception

This is where Modelo 721 gets interesting. The law specifically targets crypto held in custody—meaning someone else (an exchange) is holding the keys for you.

If you use self-custody—like a hardware ‘cold wallet’ (Ledger, Trezor) or a private software wallet where you hold the private keys—you generally do not have to file Modelo 721. Why? Because technically, those assets aren’t ‘held abroad’ by a third party; they are in your personal possession. However, be careful: if you move that crypto back to an exchange before December 31st and it’s worth over €50k, the obligation returns!

4. Filing Deadline

- Deadline: Model 721 must be filed between January 1st and March 31st of the year following the year to which the information refers.

In Summary (Two Primary Requirements for Filing):

- The virtual currencies must be custodied by a third party providing services to safeguard the cryptographic keys (i.e., held in a custodial wallet or on an exchange).

- That custodial entity must not be a resident in Spain or a permanent establishment in Spanish territory.

How is the AEAT Policing Crypto-to-Crypto Swaps

In 2026, the Spanish Tax Agency (AEAT) treats every single interaction with cryptocurrency as a potentially taxable event. For those under the Beckham Law, the rules are uniquely complex because of the “source of income” debate.

Here is the breakdown of how the AEAT is policing crypto-to-crypto swaps and the specific risks for Beckham Law beneficiaries.

1. The “Swap” Trap: Why It’s Taxable Even Without Cash

In Spain, cryptocurrency is not considered “money” but a digital asset (similar to a piece of property).

- The Rule: Every exchange (e.g., swapping Ethereum for Bitcoin) is viewed as two separate transactions:

- A Sale of Asset A at its current Euro market value.

- An Acquisition of Asset B at that same Euro market value.

- The Consequence: You must calculate the capital gain or loss in Euros for every single trade. Even if you never “cashed out” to a bank account, you owe tax on the gain generated during that swap.

- Calculation Method: Spain strictly uses the FIFO (First-In-First-Out) method. The AEAT assumes you are selling the very first units of that specific coin you ever bought, which often leads to the highest possible taxable gain.

2. Beckham Law: The “Source” Conflict

The primary benefit of the Beckham Law is that you only pay tax on Spanish-source income. However, the AEAT is aggressively redefining what “Spanish-source” means for crypto:

- Foreign Exchanges: Generally, if your crypto is held on a platform based outside of Spain (e.g., Binance Jersey, Coinbase US), gains from swaps are considered foreign-source and are exempt from tax under the Beckham Law.

- Spanish Exchanges: If you use a Spanish-based exchange (like Bit2Me), the income is considered Spanish-source and you must pay a flat 24% (or the savings scale of 19%–28%, depending on the specific filing year’s interpretation) even under the Beckham Law.

- The “Private Key” Risk: Recent binding rulings suggest that if you hold the private keys (Cold Wallet) while physically living in Spain, the AEAT may argue the asset is “located” in Spain. This would make all gains taxable at the standard rates, potentially stripping away the Beckham Law exemption for your crypto portfolio.

3. Staking and Mining (General Income vs. Savings)

If you are earning new tokens through Staking or Mining, the AEAT classifies this as General Income (Rendimientos del capital mobiliario), not capital gains.

- Standard Residents: Pay progressive rates up to 47%.

- Beckham Law: If the staking is performed on a foreign platform, it is usually exempt. However, if the AEAT determines the “activity” is managed by you from your desk in Madrid, they may label it “Spanish-source entrepreneurial activity,” making it taxable at 24%.

How the AEAT Catches Discrepancies in 2026

Under the DAC8 Directive, the AEAT receives an automatic data dump from global exchanges every month. This includes:

- Your Tax ID (NIE).

- Total value of swaps performed.

- Year-end balances.

If you are under the Beckham Law and the AEAT sees millions in swaps on your NIE but €0 declared, they will open a “Verification of Data” (mini-audit) to ask you to prove those exchanges were truly foreign-sourced and not managed through a Spanish “Permanent Establishment.”

Modelo 151 & Modelo 721

It is crucial to understand that these two obligations have different “jobs” for the tax inspector:

1. Beckham Law (Modelo 151) – The “Income” Side

- What goes here: You report any capital gains from swaps that are Spanish-sourced.

- The Conflict: If you trade on a Spanish exchange, you must pay tax here. If you trade on a foreign exchange (Binance/Coinbase), it is technically exempt.

- The PE Risk: If the AEAT proves you have a Permanent Establishment (because you trade 8 hours a day from Madrid), they will claim the “source” of your global crypto gains is actually Spain. This would not only make all those gains taxable at 24% but could cancel your Beckham Law status entirely, back-taxing you as a regular resident at rates up to 47%.

2. Modelo 721 – The “Evidence” Side

- What goes here: This is just a list of what you hold abroad (if you are a regular resident).

- Why it matters for Beckham Law users: Even though Beckham Law users are technically exempt from the 720/721 reporting, the DAC8 data dump means the AEAT already knows your transaction volume.

- The Trap: The AEAT uses the data that would go in a 721 to build a case for your Beckham Law audit. For example: “We see 5,000 trades on Binance Jersey via DAC8. This person is clearly a professional trader operating from a desk in Barcelona. Therefore, they have a PE and don’t qualify for the Beckham Law.”

Summary Table for 2026

| Issue | Impact on Beckham Law (M151) | Relation to Modelo 721 |

| Swaps | Taxable if Spanish-source; Exempt if foreign-source. | Changes your balance; triggers DAC8 reporting by the exchange. |

| PE Risk | High. Could disqualify you from the flat 24% rate. | Your trading volume is the evidence they use to prove a PE exists. |

| Staking | Usually exempt if foreign; taxable if the activity is “managed” in Spain. | Must be declared as a “holding” if tokens stay on the exchange. |