How to Fill Out Spanish Form 210: Complete Non-Resident Tax Guide in English & Spanish

Here is a clear and simple summary of how to fill in Form 210 for non-residents in Spain, based on the official instructions.

1. Who Must File Form 210?

You must file if you are a non-resident without a permanent establishment in Spain and you receive income that was not subject to withholding tax or where withholding was insufficient. Common situations include:

- Rental Income: When your tenant is an individual (not a company) and does not withhold tax.

- Imputed Income (“Renta Imputada”): For owning a Spanish property that is not your primary residence and is not rented out. You pay tax on a theoretical rental income.

- Capital Gains from Selling Property: You must file to calculate the final tax, even if the buyer withheld 3% at the sale. This can result in a payment or a refund.

- Capital Gains from Selling Shares/Assets: When the buyer did not withhold tax.

- Requesting a Refund: If too much tax was withheld (e.g., on dividends, sale of property).

2. When to File (Deadlines)

| Type of Income | Filing & Payment Deadline |

|---|---|

| Sale of Spanish Property | Within 3 months after the 1-month period following the sale date. |

| Imputed Income (Property Ownership) | From January 1 to December 23 of the year following the tax year (e.g., for 2023 income, file in 2024). |

| Other Income (Rent, Dividends, etc.) – Result is a PAYMENT | First 20 calendar days of April, July, October, and January for income from the previous calendar quarter. • For rental income from 2024 onward: You can choose to group it annually and file in the first 20 days of January of the following year. |

| Zero or Refund Result | From February 1 of the following year, within a 4-year deadline. |

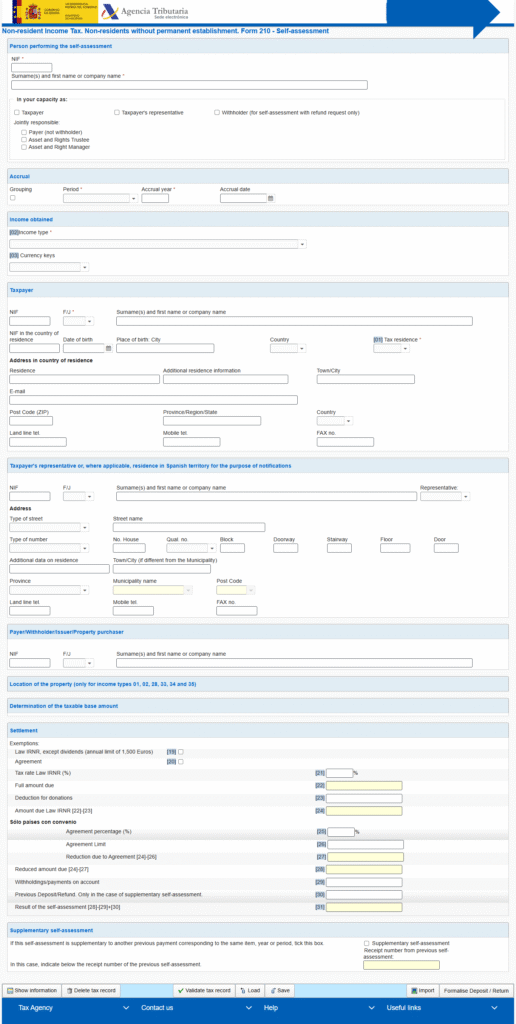

3. How to File: Step-by-Step Guide

You can file online (recommended) via the Spanish Tax Agency’s website with a digital certificate/Cl@ve, or on paper.

📄 Need an official form? > You can download the reference PDF and other tax models in our Spanish Tax Forms Library. We provide summaries and official BOE templates to help you prepare your filing.

Key Sections to Complete:

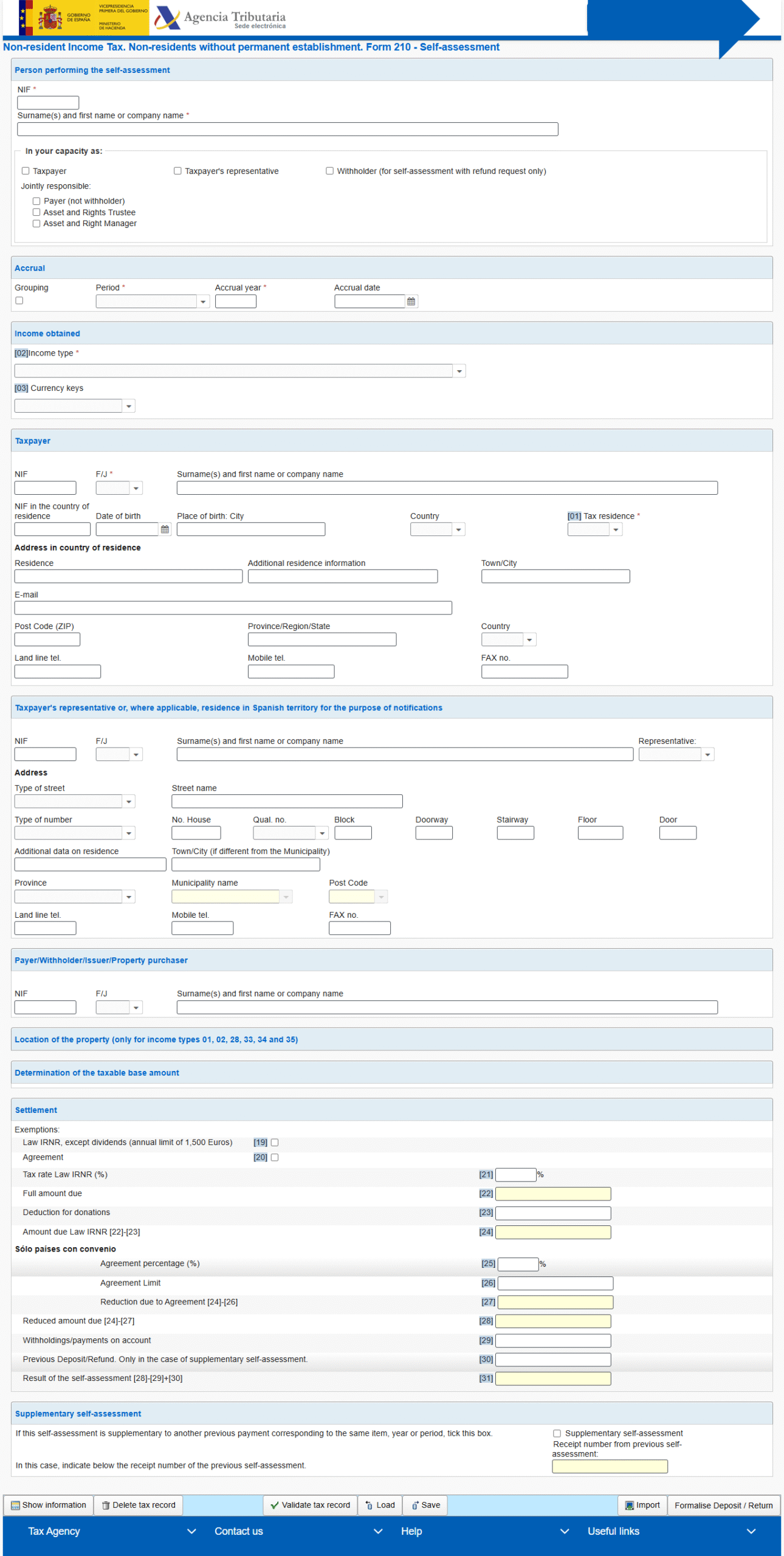

A. Top of the Form (Datos Comunes)

- Person completing the form: Your details if you are the taxpayer or your representative’s.

- Taxpayer (Contribuyente): Your personal information as the non-resident.

- NIF: Your Spanish tax ID (NIE).

- Surname, Name: Your full name.

- Country of Tax Residence: Your current country of tax residence code.

- Address: Your full foreign address.

B. Income Details (Datos de la Autoliquidación)

- Type of Income (02): This is the most important box. Select the correct code from the list (see summary table below).

- Accrual Date: The date you received the income or when the sale occurred.

- For Property-Related Income: You must provide the Cadastral Reference of the property.

C. Select the Correct Calculation Section (I, R, H, or G)

Only fill out ONE of these sections based on your income type.

| Section | Use For… | Key Boxes to Fill |

|---|---|---|

| 210 I | Imputed Income from owning a vacant/second home. | (4) Tax Base: Cadastral Value x 1.1% (if revised after 2012) or x 2%. |

| 210 R | Actual Income: Rent, dividends, interest, etc. | (5) Total Income: Full amount received. (8) Tax Base: Usually the same as (5). |

| 210 H | Capital Gains from Selling Property. | (9) Sale Price (minus costs). (10) Purchase Price (plus costs). (12) Profit: The taxable gain (may be reduced for properties bought before 1994). |

| 210 G | Other Capital Gains (e.g., from selling shares). | (18) Tax Base: Profit from the sale (Sale Price – Purchase Price). |

D. Settlement (Liquidación)

- Tax Rate (21): Enter the applicable rate.

- 19% for residents of the EU, Iceland, Norway, or Liechtenstein.

- 24% for all other countries.

- (Other specific rates apply to dividends, pensions, etc. – see fact sheet).

- Withholdings/Payments on Account (29): Enter any tax already withheld (e.g., the 3% from a property sale, or 19% on dividends).

- Result (31): This is the final amount. A positive number means you pay. A negative number (with a minus sign -) means you get a refund.

4. Essential Documentation to Attach

- Certificate of Tax Residence: From your country of tax residence, if you are applying a Double Taxation Treaty benefit or an EU exemption.

- Proof of Withholding: If claiming a refund for excess withholding.

- Proof of Property Ownership & Cadastral Reference: For property-related filings.

- Bank Details (IBAN/BIC): For refunds, a certificate of account ownership.

- Power of Attorney: If a representative is filing for you.

5. Quick Reference: Common Income Type Codes (Box 02)

| Code | Description |

|---|---|

| 01 | Rental income from one property/tenant. |

| 02 | Imputed income from property ownership. |

| 04 | Dividends. |

| 05 | Interest. |

| 28 | Capital gain from selling property. |

| 35 | Rental income grouped from multiple properties/tenants (from 2024). |

Summary Checklist

- ✅ Determine if you must file (no withholding or special cases like property).

- ✅ Identify your income type and get the correct code (02).

- ✅ Gather all supporting documents (NIE, residency certificate, property details, proof of income/costs).

- ✅ Calculate your taxable base in section I, R, H, or G.

- ✅ Apply the correct tax rate (19% or 24% generally).

- ✅ Deduct any withholding already paid.

- ✅ Calculate the final amount to pay or be refunded.

- ✅ File online (recommended) by the deadline or submit paper forms to the correct office.

Disclaimer: This guide is a simplified summary for informational purposes. Tax rules are complex. For your specific situation, it is highly recommended to consult with a Spanish tax advisor (gestor) or lawyer specialized in non-resident taxation.

{kind=link}

{kind=link}