IAE (Economic Activities Tax) and Choosing the Right Epígrafe

The IAE code choice defines an Autónomo’s tax obligations (e.g., whether they must withhold IRPF). This post solves the initial registration dilemma.

The IAE’s Role

The Impuesto sobre Actividades Económicas (IAE) is a local business tax that must be declared by every self-employed worker, even if they are exempt from paying the fee.

The primary function of the IAE is not to collect revenue from small autónomos, but rather to serve as a census and classification tool. Your selected Epígrafe (code) officially defines the nature of your activity for the Spanish Tax Agency (AEAT).

| IAE Key Fact | Detail | Implication for Expats |

| Mandatory Registration | Every economic activity must be registered via a specific numerical code (Epígrafe) on Modelo 036/037. | You must choose your Epígrafe before you start invoicing. You can select multiple codes if you perform various activities. |

| Tax Exemption | The IAE fee is 100% exempt for the first two years of activity and for all taxpayers with net turnover below €1,000,000. | This means virtually all expats pay €0 in IAE fees, but registration is still mandatory. |

| Code Type Matters | The Epígrafe determines if you are categorized as a Professional or a Business activity. | Professional codes (Groups 2 & 3) require you to withhold IRPF (usually 7% or 15%) on invoices to Spanish businesses, while Business codes generally do not. |

Navigating the Code Search

The process of selecting the correct Epígrafe (code) is a compliance hurdle for all self-employed workers.

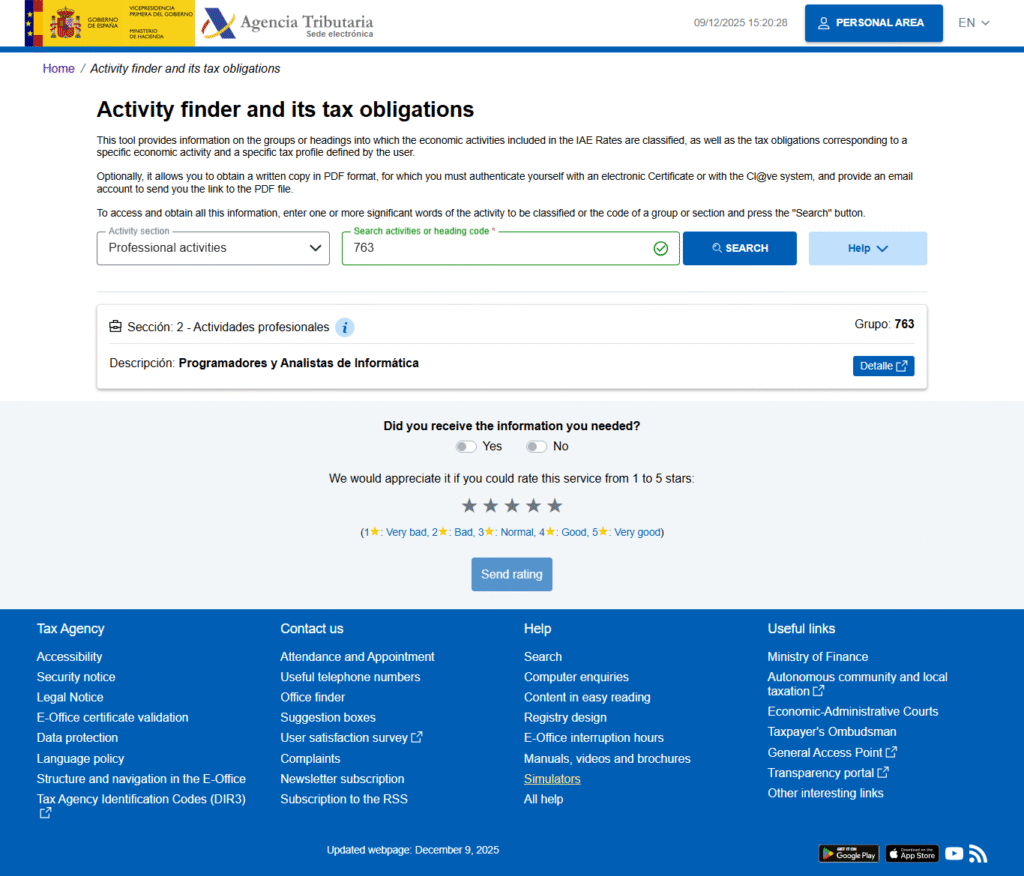

Search the IAE List: Use the AEAT’s official IAE search tool (Buscador de Epígrafes) by entering keywords related to your activity (e.g., “programmer,” “consulting,” “designer”).

🔗 Official AEAT Tool: Buscador de Epígrafes IAE (You may need to search the AEAT site directly as the link can change).

Hre you have available to download the activities classification list.

Professional vs. Business: For freelancers (like programmers, marketers, consultants), the choice is often between a Professional code (e.g., 763: Programadores y Analistas de Informática) and a Business code (e.g., 844: Servicios de Publicidad).

💶 Crucial Implication: IRPF Withholding

The most significant immediate consequence of your IAE code choice for a self-employed person is its effect on your Impuesto sobre la Renta de las Personas Físicas (IRPF)—or Personal Income Tax—obligations.

When must you withhold IRPF?

If your activity is classified as Professional (Section 2), you are legally required to include an IRPF withholding (known as retención) on any invoice issued to another Spanish business or autónomo.

- General Rate: The standard withholding rate is 15%.

- Reduced Rate: For new autónomos, a reduced rate of 7% can be applied during the first three calendar years of activity.

The client then pays this withheld amount directly to the AEAT on your behalf. This is essentially an advance payment of your annual income tax.

When should you not withhold IRPF?

- If you choose an Business (Section 1) Epígrafe.

- If you issue an invoice to a non-Spanish entity (a business or client outside of Spain).

- If you issue an invoice to a private individual (not a business or autónomo).

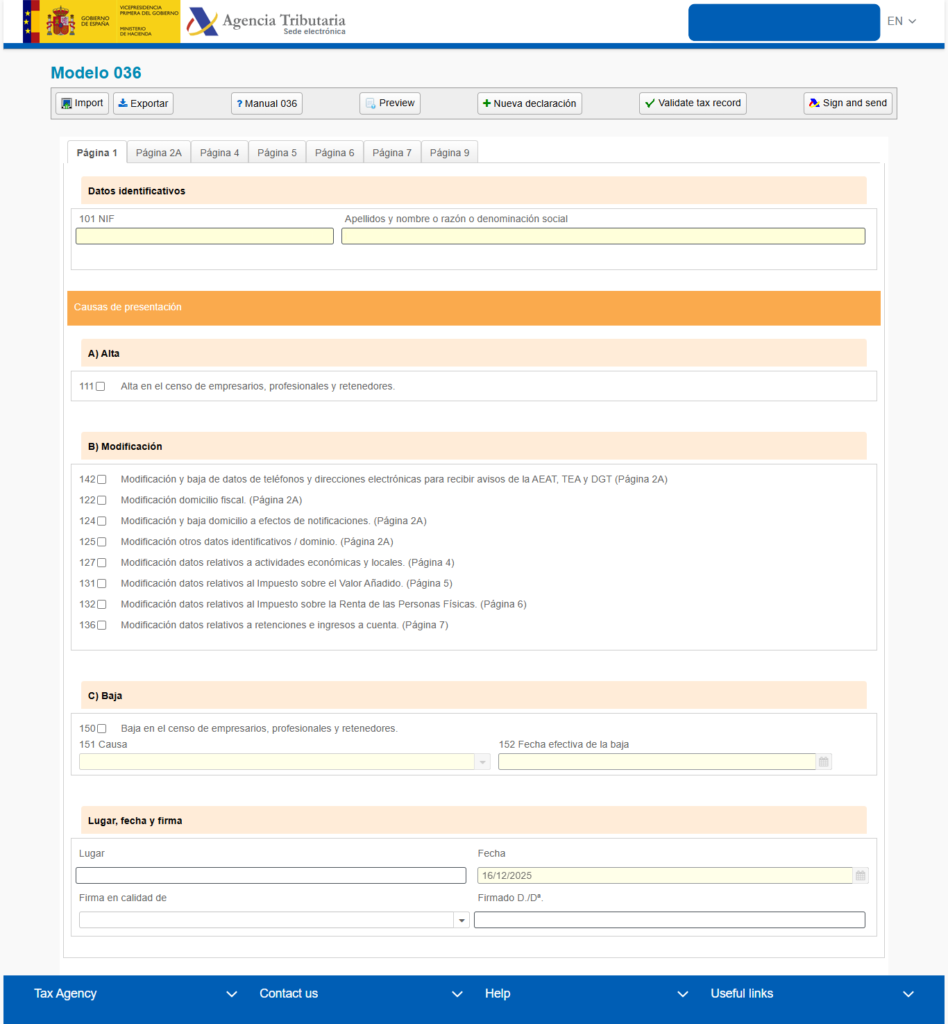

The Censal Declaration (Modelo 036/037)

The IAE code is declared when you register your activity with the AEAT, which is done through the Censal Declaration. This is the official document that informs the Tax Agency about the start, modification, or cessation of your activity.

- Modelo 037 is the simplified form for most autónomos.

- Modelo 036 is the standard form, used for more complex scenarios (like setting up a company or having multiple locations).

- 🔗 Official AEAT Document: Modelos 036 y 037 – Declaración censal

Choosing the correct code and understanding your corresponding IRPF obligations from the start is paramount to avoiding future penalties from the AEAT.

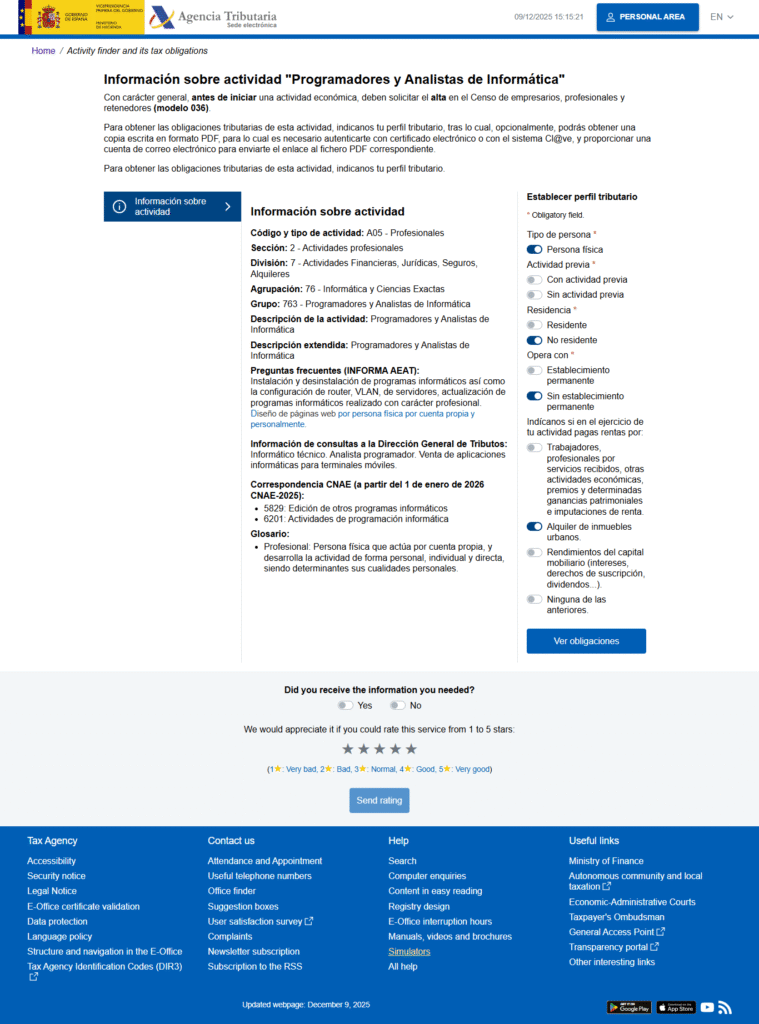

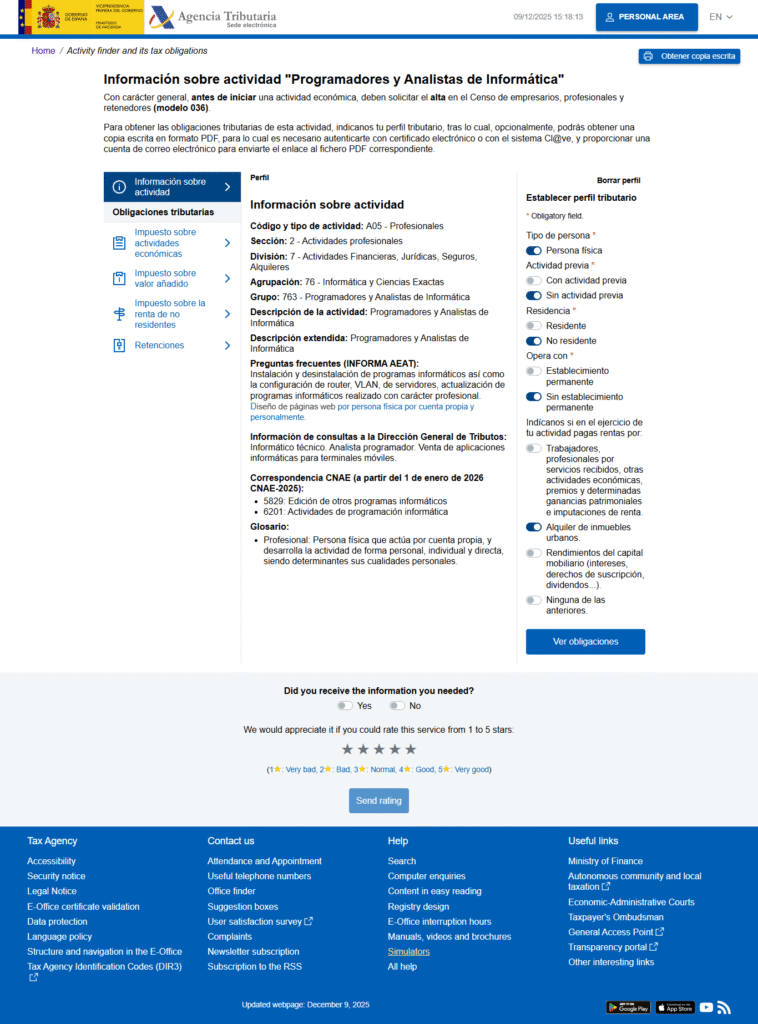

IAE Examples for with 763 Epígrafe

On picture 1 you choose your Epígrafe. On picture 2 they show you some options to click according to your situation. On picture 3, at the left, you can click to find out your obligations regarding registration or taxes.

💻 IAE Examples for Digital Professionals

The primary challenge for digital autónomos is that the IAE list is dated, and modern jobs often require using a proxy or combining codes. The choice determines if you must withhold IRPF.

1. Web Designer / Developer

For an individual, freelance Web Designer or Developer, the activity is typically classified as Professional (Section 2) because it relies on personal, technical expertise.

| Activity | Recommended Professional IAE Code (Section 2) | Classification | IRPF Withholding |

| Web Designer (focused on coding/programming/analysis) | 763 – Programadores y Analistas de Informática (Programmers and Computer Analysts) | Professional | Required (15% or 7% for new autónomos) |

| Graphic Designer (focused on visual arts, not coding) | 399 – Otros profesionales relacionados con… (Other related professionals…) or 751 – Diseñadores (Designers) | Professional | Required (15% or 7% for new autónomos) |

💡 Tip: Most freelance web professionals register under 763 as it clearly covers the technical programming/development aspects of the job.

2. Marketing Consultant / SEO Specialist

This category is often the most confusing because marketing can be classified as either Professional (individual service) or Business (structured agency service).

| Activity | Recommended IAE Code | Section | IRPF Withholding |

| Marketing Consultant (Personal, direct advisory service) | 843 – Profesionales relacionados con la publicidad, relaciones públicas y similares (Professionals related to advertising, public relations, and similar) | Professional (Section 2) | Required (15% or 7% for new autónomos) |

| Marketing Agency (Using a complex structure, personnel, or means) | 844 – Servicios de publicidad, relaciones públicas y similares (Services of advertising, public relations, and similar) | Business (Section 1) | Not Required |

⚠️ Key Difference: If you choose the Business code (844), you generally do not have to apply IRPF withholding on your invoices. This is a common strategy, but it must be justified by the existence of a minimal business structure (even if it’s just equipment and a dedicated home office).

📋 The Registration Process Summary

The IAE code is one part of the initial registration process. You must submit your Censal Declaration (Modelo 036/037) to the AEAT and your Social Security registration (Modelo TA0521) to the Seguridad Social.

| Step | Purpose | Form | Authority |

| 1. Tax Registration | To declare your activity, IAE code, and tax obligations (IRPF/IVA). | Modelo 036/037 | Agencia Tributaria (AEAT) |

| 2. Social Security | To register in the RETA (Special Regime for Self-Employed Workers). | Modelo TA0521 | Seguridad Social (TGSS) |

- 🔗 AEAT Official IAE Search Tool: Buscador de Epígrafes IAE

- 🔗 AEAT Censal Declarations (Modelo 036/037): Modelos 036 y 037 – Declaración censal

- 🔗 Seguridad Social Form (Modelo TA0521): Alta en el RETA (Self-Employed Registration)

💰 IAE and Deductible Expenses (IRPF)

That is a critical point! While the core rules for deducting expenses are generally the same for all autónomos under the Estimación Directa (Direct Estimation) tax regime (which is what most freelancers use), the legal requirements and certain specific deductions can differ slightly based on whether you are classified as Professional (Section 2) or Business (Section 1).

Here is a breakdown of the differences in expense deduction and accounting obligations:

The key principle for all autónomos remains the same: A cost is deductible if it is “necessary for the income-generating activity” (correlación con ingresos), properly justified, and recorded.

| Feature | Professional Activity (Section 2) | Business Activity (Section 1) |

| Accounting Books | Mandatory: Sales, Purchases, Investment Goods, and Provisions and Expenditure Items (Book 4). | Mandatory: Sales, Purchases, and Investment Goods. |

| Specific Deductions | Deduction Limit: Cannot deduct provisions for general expenses (Book 4 is to track this). | Deduction Limit: Can deduct certain provisions, such as for bad debts (pérdidas por insolvencia), which are not generally available to professionals. |

| Home Office Supplies (Suministros) | Identical Rule: If you work from home, you can deduct a percentage of home utilities (electricity, water, gas, internet) based on the percentage of your home dedicated to work, and then applying a 30% reduction to that amount. | Identical Rule: Same 30% rule applies. |

| Social Security Fee (Cuota de Autónomos) | Identical: The entire monthly Cuota de Autónomos is fully deductible as an expense in the IRPF declaration. | Identical: Fully deductible. |

| Client Invoicing | Mandatory IRPF Withholding on invoices to other Spanish businesses. | No IRPF Withholding on invoices. |

The Core Difference: Accounting Books

The main distinction for small autónomos operating under the Simplified Direct Estimation (Estimación Directa Simplificada) lies in one of the required accounting books:

- Professionals (Section 2) must keep a Book of Provisions and Expenditure Items (Libro Registro de Provisiones y Gastos). This is to track specific legal provisions (like for professional obligations or retirement funds) which are generally more limited than those available to large businesses.

- Business Owners (Section 1) generally do not need this specific book, but may be able to deduct provisions for risks and expenses allowed under general commercial law, though this is rare for small autónomos under the simplified regime.

Conclusion for the Freelancer: For the average expat freelancer who has low structural costs and works from home, the difference in the amount of deductible expenses is minimal. The decision between Professional and Business codes is almost always driven by the IRPF withholding obligation (as covered in the previous section), not by expense deduction rules.

The “Hidden” Rule: Why you (likely) don’t need Modelo 840

In Spain, all natural persons (individuals/autónomos) are legally exempt from paying the IAE tax. Because you are exempt, you generally do not use Modelo 840 for your registration.

Instead, you use Modelo 036 or 037 (the Census Declaration). When you pick your IAE heading (epígrafe) on those forms, you are fulfilling your registration obligation.

When Modelo 840 MUST be on your checklist

You only need to worry about Modelo 840 if you fall into one of these specific “High-Earner” or “Corporate” scenarios:

- The €1 Million Threshold: If your net turnover (INCN) exceeds €1,000,000 in a year, you lose your exemption. You must then file Modelo 840 to officially register for the tax.

- Becoming a Legal Entity: If you move from being an individual autónomo to forming a company (Sociedad Limitada), the company is exempt for the first 2 years. After that, if it earns over €1M, Modelo 840 becomes mandatory.

- Local Variations: Some specific municipalities require it for communicating changes in physical business premises (square footage, power usage) if those elements affect local tax calculations, though this is increasingly handled via the 036.

Summary of Deadlines (If you trigger the requirement)

| Situation | Deadline |

| Starting Activity (as a non-exempt entity) | Within 1 month of starting. |

| Losing Exemption (e.g., you hit €1M turnover) | During the month of December prior to the year you must start paying. |

| Changes/Variations (address, power, etc.) | Within 1 month of the change. |

| Ceasing Activity | Within 1 month of the end of activity. |

Tip: If you are a standard freelancer earning under €1M, you can safely stick to Modelo 036/037. Hacienda already knows your IAE status through those forms.

{kind=link}